- Overview of crowdfunding in Italy 2023-2024

- Crowdfunding platforms and the ECSP Regulation

- The declining of equity crowdfunding

- The path of companies after equity crowdfunding

- The growing of lending crowdfunding and debt crowdfunding

- The peculiarities of real estate crowdfunding

- Who is doing crowdfunding in Italy?

- A look at donation and reward crowdfunding

- Want to learn more directly with our crowdfunding experts about the topic you are reading about?

- Do you need support in preparing a successful crowdfunding campaign and seeking potential investors for your project?

In July each year, the Crowdinvesting Observatory of the Politecnico di Milano publishes an annual report on crowdfunding market trends in Italy. The 2024 report has just been released and is the first after the concrete start of the implementation of the ECSP Regulation, the European regulation that has standardized crowdfunding rules in the various EU member states. This introduces new variables to analyze and new perspectives to consider.

Overview of crowdfunding in Italy 2023-2024

The report's data focus on crowdinvesting segments, or those forms of crowdfunding that give campaign participants the opportunity to earn a return of capital: lending, equity and debt crowdfunding.

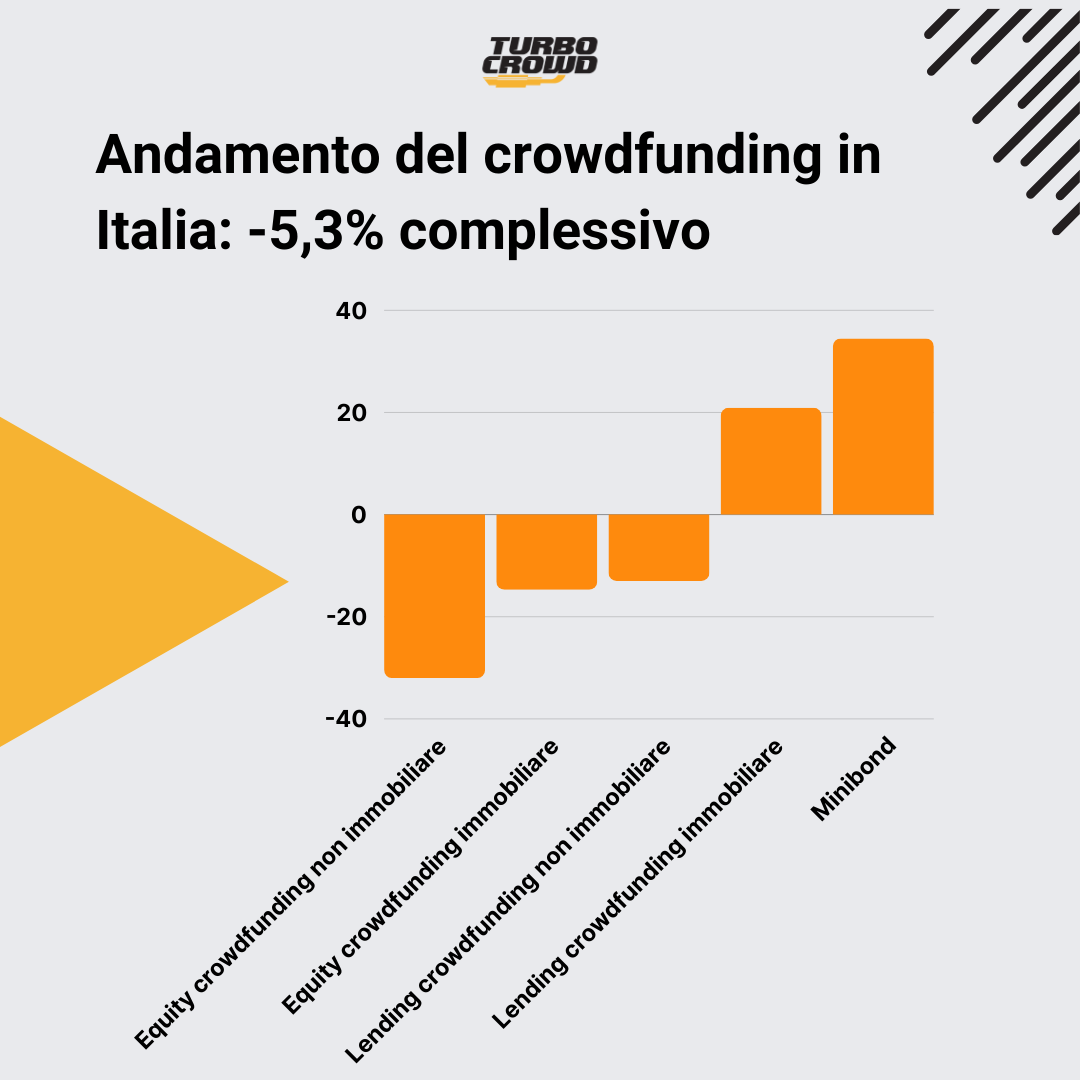

Considering these three main types of crowdfunding, for the second year in a row the Italian market suffered an overall decline, this year more pronounced: -5.3 percent. Total fundraising was €302.35 million, down from €343.79 in the previous 12 months.

Equity crowdfunding is mainly responsible for the decline again this year, while lending crowdfunding continues to grow. It remains driving, in both types, the real estate sector. Finally, the exploit of minibonds (debt crowdfunding) is surprising, and after last year's poor performance they are making a strong recovery.

The report identifies as one of the likely causes of this decline the slow pace of authorization of platforms under the ECSP Regulation and the complexity of the new regulatory standard: many platforms have been forced to halt operations for weeks or months while waiting for Consob and Bank of Italy verifications on compliance with the new regulation and subsequent authorization to operate; many have had to close due to the inability to sustain compliance; and some others have been incorporated by larger players.

In contrast, the success rate of campaigns remains stable, and very positive, at around 90 percent for all types.

Crowdfunding platforms and the ECSP Regulation

The ECSP Regulation has given crowdfunding platforms a hard time, but the slowness and confusion of the Italian competent authorities has also played its decisive role in complicating the lives of crowdfunding service providers.

In fact, the regulation was approved as early as 2021, but took 2 years to be transposed by the slowest EU countries (including Italy), and still until spring 2023 Italy had not chosen the competent authorities that would be responsible for authorization and supervision for the implementation of the regulation.

Once designated, Consob and Banca d'Italia took additional time to determine how to apply for authorization, so platforms had little time to organize and adapt to the new requirements. Accomplice also to the slow analysis of applications by the two authorities, the result was that by November 10, 2023, the date after which unauthorized platforms could no longer operate, only 10 platforms in Italy had received authorization. There was, therefore, a forced suspension of the activities of many portals, either for weeks or for months.

As of June 30, 2024, there were 33 authorized crowdfunding platforms in Italy : we rank second in Europe after France. Yet last year there were 66 platforms surveyed. Missing from the roll call are 27 equity and 16 lending platforms, which either have not seen fit to apply for authorization under the new ECSP Regulation or may still be in the application phase for authorization. There is no hard data on this, but from information gathered by the Polytechnic Observatory, it appears that at least 20 platforms have given up applying for licensing, while about 10 are waiting.

The foreign platforms that have applied for and been granted permission to operate in Italy, however, at present are Crowdcube (UK), Urbanitae (Spain), Seedrs (UK), Crowdestate (Estonia) and Housers (Spain).

The declining of equity crowdfunding

Equity collection between July 2023 and July 2024 was 106.53 million euros, which corresponds to a decrease of -25.5 percent compared to the previous twelve months. Not only the capital raised, but also the number of closed campaigns decreased.

The deepest decline was in campaigns on non-real estate projects (-32%), while real estate equity campaigns held up and raised the most. The average collection value for non-real estate campaigns was €208,794, for real estate campaigns €1,155,826.

According to the report, “weighing on the performance of the equity crowdfunding market are rising interest rates that have made traditional forms of investment such as bonds and government securities more competitive and attractive, uncertainty over the economy (especially with respect to geo-political tensions), and the suspension of operations of many portals at the beginning of November 2023 pending ECSP approval.”

Despite this negative trend, platforms have been more selective in their choice of campaigns to host, favoring companies and projects with good membership potential and able to demonstrate the ability to leverage their own contacts accumulated and cultivated over time. This removes any doubt that it is the companies that should be in charge of bringing investors to the platform, and not the platforms that get investors to the companies. This is why it is so important to learn how to do lead generation, how to build and cultivate a community, and to do all of this before you do a crowdfunding campaign, not after, not during.

A final interesting fact is that the average value of investors in equity crowdfunding campaigns is 95.8 (median value 58).

Finally, we highlight that the first two campaigns for the placement of Participatory Financial Instruments, which the ECSP Regulation made possible on crowdfunding platforms, were also carried out.

The path of companies after equity crowdfunding

The Polytechnic report offers an important reflection on the path of companies that have campaigned on equity crowdfunding and identifies the large number of entities that fail to reach their goals as another cause of the declining desirability of this financial instrument.

After the campaign, a few companies manage to grow, some even go as far as listing on the stock exchange or become the protagonists of major mergers, but most simply survive. It should be noted that for innovative startups, which make up a large share of equity issuers, it is normal not to see positive margins and profits in the early years, but the observed figure remains relevant.

As we had already pointed out when commenting on the 2023 report, an equity crowdfunding campaign is only a beginning and must be embedded in a broader strategy of marketing and sales, systematic capital raising, and networking.

Want to learn more directly with our crowdfunding experts about the topic you are reading about?

Turbo Crowd can reveal to you all the tricks of the crowdfunding trade, explain the capital-raising opportunities available to you, and provide you with practical support to carry out a successful crowdfunding campaign.

The growing of lending crowdfunding and debt crowdfunding

Perhaps the most astonishing figure in this year's report is the +34% increase recorded by Minibond placements, which even surpassed nonreal estate lending. This large increase is partly due to last year's terrible performance, and partly due to the fact that ECSP Regulation has lifted restrictions on Minibond purchases for retail investors. The need for special authorization for portals to place this type of debt securities also falls: the 19 campaigns completed in the past year were on only 2 portals (Fundera and Opstart), but more portals are expected to be dedicated to Minibonds as well.

Lending crowdfunding continues with its unstoppable positive trend (+7.7%) and remains a popular tool for businesses and investors because of its versatility. The average interest rate was 9.82 percent and the average loan maturity 15 months. Finally, most companies opt for a bullet repayment of the loan (full repayment at maturity).

The peculiarities of real estate crowdfunding

Real estate crowdfunding always deserves its own paragraph, because it is a now well-defined phenomenon with distinctive features. For all types of crowdfunding, it is the leading sector, indeed decisive for positive signs and the only one that can mitigate negative signs.

Real estate crowdfunding projects recorded an overall +7.2%, which stems from +20.9% in lending crowdfunding and -14.7% in equity.

We explained in the article on real estate crowdfunding why the lending type is particularly congenial to this type of project.

As the report summarizes, “Typically, these are short-to-medium-term projects that aim to redevelop (or build from scratch) and subsequently dispose of real estate; [...] crowdfunding has an important boost role in initial financing due to the speed of collection and the absence of collateral.”

From an investor's perspective, real estate crowdfunding is particularly attractive because it overcomes the traditional obstacles of investing in brick and mortar: the need for large resources, administrative and management burdens, low liquidity, and the low possibility of diversification.

Real estate crowdfunding offers “opportunity to participate in a project with low amounts of money; opportunity for diversification, as by lowering the capital required for the individual investment each individual can invest in a greater number of projects, [...] delegation of property management to the project developer.”

That is why as many as 11 of the 15 lending crowdfunding platforms active in Italy are vertical on real estate.

Who is doing crowdfunding in Italy?

Let us conclude with a quick look at the characteristics of the actors in the crowdfunding industry. Of the platforms we have already talked about, let us now see who are the initiators of campaigns and the investors who participate in them.

Crowdfunding companies are 60% startups and the remainder mostly SMEs. Almost all of them are LLCs. This year, for the first time, in equity crowdfunding the percentage of startups fell below 50 percent, showing a greater interest of even older companies in the tool.

Most of the companies operate in Lombardy and are active in information and communication services.

As for investors, the data concern equity crowdfunding only and note a deep gender gap, with only 16 percent female investors, and a prevalent age between 30 and 50. As usual, the report points out that “the vast majority of investors [...] chose only one campaign (many of these probably belong to the entrepreneur's personal network of contacts).”

It is interesting to compare these data with some of those that emerged in the European report from earlier this year to which we devoted an article.

A look at donation and reward crowdfunding

Although the report focuses on equity and lending crowdfunding, it always devotes a brief overview to the two types outside crowdinvesting: donation and reward crowdfunding.

There are 22 portals active in the donation and reward areas, raising a total of 51.7 million euros in the past 12 months. Among the most active are ForFunding, Eppela and Produzioni dal Basso.

Donation campaigns are mainly about fundraising for tragic events such as the floods that hit Emilia-Romagna last year; reward campaigns are mainly aimed at financing art projects, recreational productions (video games, board games, etc.) and technological products.

Do you need support in preparing a successful crowdfunding campaign and seeking potential investors for your project?

Turbo Crowd can accompany you throughout the process, from organizing the precrowd to closing the collection, developing effective and innovative marketing strategies to best promote your campaign.