- How lending crowdfunding works

- Who can do lending crowdfunding

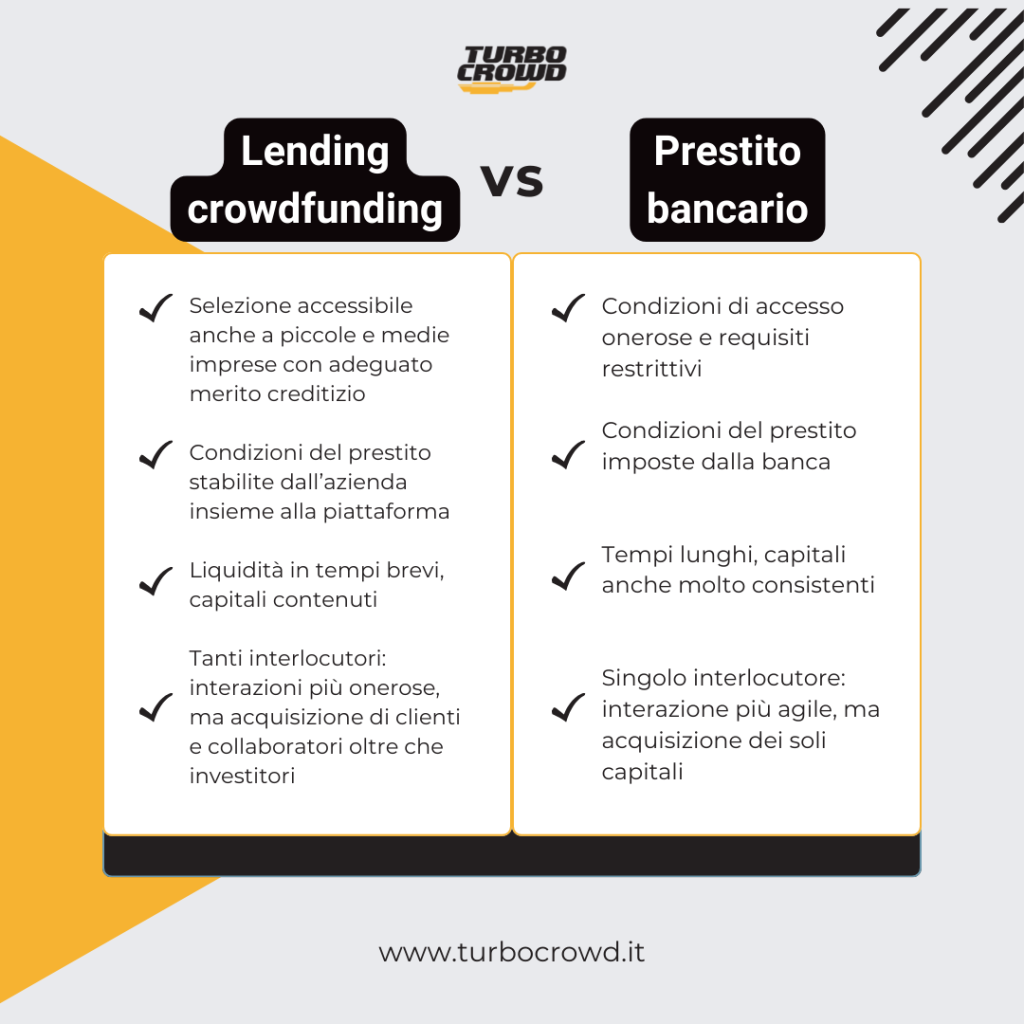

- Why do lending crowdfunding? The advantages

- Time and costs

- The regulations

- Real estate lending crowdfunding

- Lending crowdfunding in Italy and Europe

- Want to learn more directly with our crowdfunding experts about the topic you are reading about?

- Do you need support in preparing a successful crowdfunding campaign and seeking potential investors for your project?

Lending crowdfunding is a form of lending between individuals, in fact it is also called peer-to-peer lending or social lending. It allows you to disintermediate credit and apply for a loan online from a multitude of individuals, rather than going to a bank.

An individual in need of financing can campaign on a specialized online platform to apply for a loan and reach the amount by raising capital from multiple lenders, who will receive interest in return.

Lending crowdfunding is thus a type of crowdinvesting, because people who participate in a campaign make an investment and get a return on their capital.

How lending crowdfunding works

Lending crowdfunding functions as a loan that is intended as an alternative financing channel to banking or other financial intermediaries. Unlike traditional lending, there is not a single party lending to another party, but a multitude of lenders ("crowd") who can be professional or retail (sophisticated or unsophisticated, according to the new European wording).

There are two models of lending crowdfunding.

- The diffused model requires would-be investors to provide the platform with some capital and indicate a risk profile and expected interest rate, and then let the portal choose the capital allocation among the available projects.

- The direct model involves would-be investors deciding for themselves which projects to invest in, viewing them on the platform and making the transaction directly.

The second model is the most common and is the one that most embodies the idea of crowdfunding, so we will refer only to it.

The crowdfunding platform, in this second model, is the meeting place between supply and demand, i.e., between the party requesting the loan and the investors financing it. At the end of the campaign, if the funding goal has been reached, the amortization plan chosen by the company to return the loan plus predetermined interest to investors begins. There are two main amortization schedules:

- Bullet (repayment of principal in a single payment at loan maturity)

- Amortizing (repayment of capital in installments).

The most commonly used mode is the former.

In turn, interest can be paid to investors in installments of fixed or variable amounts or in a single payment when the loan matures.

Who can do lending crowdfunding

We spoke generically of "subject" referring to lending crowdfunding borrowers, because a peculiarity of this financial instrument is that it is open to everyone.

Not only businesses, but also individuals can apply for a loan through a lending crowdfunding campaign, as long as they are of legal age, have a demonstrable income, and no serious history of default. Platforms that deal specifically with lending to individuals are called "consumer." Consumer lending crowdfunding, however, is uncommon and the portals that deal with it tend to be absorbed by traditional financial institutions, so we will not discuss it in this article.

For businesses, however, it is referred to as lending crowdfunding business. There are no type or size limitations: not only startups or SMEs, but all businesses can access lending crowdfunding. With the effective implementation of the European ECSP regulation, this is now also the case for equity crowdfunding, which was previously reserved for innovative startups and SMEs.

The selection of proposing companies made by lending crowdfunding platforms prefers companies that have a certain historicity, so at least a financial report, turnover figures, or a rating: elements to assess the debt sustainability and risk level of the possible loan.

For this reason, lending crowdfunding is not suitable for fledgling startups, but it is aimed at businesses that are already a minimum of structure and can be useful for large companies as well. In the next section we will look at the reasons why to choose it.

Why do lending crowdfunding? The advantages

The main advantage of lending crowdfunding for a company is the ability to receive financing in a much shorter time than the average time it takes to obtain a bank loan, and with fewer conditions attached. The price to be paid is usually higher interest than the average bank rate, but the speed and flexibility of lending crowdfunding as a financing tool makes it possible to arrange dynamic capital flows and give a boost to the company's activities such that the expense is offset.

The other advantages are those intrinsic to the crowdfunding mechanism:

- The possibility of involving third parties in an entrepreneurial project who become not only investors, but perhaps also customers, collaborators, or simply testimonials who bring in other investors (analogous to "smart money" dynamics).

- Using an angle of attack that is different from competitors, which allows you to build a marketing strategy with an edge, meaning more visibility, uniqueness and unique offerings.

- The opportunity to put in place marketing and sales processes that will be a long-term asset.

- The possibility of using rewards as leverage to turn customers into investors.

Instead, what are the purposes for which this type of loan proves useful?

- Complex operations: for complex operations consisting of multiple phases of activities with cadenced timelines, it is very useful to be able to access liquidity quickly to get a crucial phase started or completed, so as not to stall the project while waiting for larger details and financing to be worked out. A prime example is real estate transactions, to which we will devote a separate section.

- Corporate loans to finance extraordinary activities (even other crowd campaigns!) or specific short-term projects or repay debts quickly.

- "Bridge" loans to have immediate liquidity while waiting for the closing of an equity crowdfunding campaign and the collection of the related principal, or the disbursement of funds from a soft finance call or other liquidity event.

- Limited involvement of a specific target group of people: for some projects it may be useful to use lending crowdfunding as a marketing tool to involve particular categories of stakeholders whose commitment is important to the success of the project itself, but without giving away shares in the company. An example is Enel's and Edison's campaigns to build renewable energy plants, which targeted the inhabitants of the areas involved.

Time and costs

Lending crowdfunding is more streamlined in terms of technical time and bureaucratic burdens than equity crowdfunding, but still requires a number of preliminary steps.

The company must first prepare the documentation with which to present itself for selection: we have devoted an article to tips for passing platform selection. Preparing these documents (business plan, balance sheet, turnover, credit history, etc.) can take from a few weeks to a few months.

The selection also varies in duration, but usually the platforms are quick and give feedback within a week. It may be necessary, however, to request additional information from the company: in this case the selection phase is prolonged.

Once the selection has been passed, the platform and company agree on the interest rate and terms of the loan to be presented to investors, then for the company's team it is time to prepare the campaign: the implementation and run-in phase of the activities to be carried out in the campaign, called precrowd, is the most important, should not be rushed, and can take from a few weeks to a few months. It is at this stage that the engagement of potential investors begins (even better if the company already has a good following and good interactions with its target audience beforehand), so that it arrives at the campaign launch with supporters ready at the starting ribbons.

Finally, the campaign itself is rather short: it usually lasts 30-45 days. After closing, if successful, loan disbursement occurs within a few days. The duration of the loan itself usually ranges from 12 to 15 months.

The costs of a lending crowdfunding campaign involve the management fees charged by the platform (which works, usually, on a success fee basis) and the expenses for the marketing activities required to bring the operation to success (advertising, media material production, consulting, etc.).

Want to learn more directly with our crowdfunding experts about the topic you are reading about?

Turbo Crowd can reveal to you all the tricks of the crowdfunding trade, explain the capital-raising opportunities available to you, and provide you with practical support to carry out a successful crowdfunding campaign.

The regulations

With the EU Crowdfunding Regulation, from the end of 2023, lending crowdfunding also has a well-defined regulation, which coincides with that for equity crowdfunding (here the differences between equity and lending crowdfunding). One small difference lies in the fact that lending crowdfunding portals can offer individual portfolio management services to users, that is, they can apply the "spread model," which does not exist in equity crowdfunding.

We have devoted an article to delving into the new features brought by this regulation, which mostly concern the transparency and investor protection obligations imposed on platforms and the possibility of raising capital abroad as well.

Real estate lending crowdfunding

Lending crowdfunding has proven so well suited to real estate transactions that crowdfunding platforms have emerged that are specifically dedicated to this (real estate crowdfunding). Real estate requires substantial resources and timeliness to close acquisitions or avoid stalling work, and lending crowdfunding addresses this need, allowing, for example, initial cash to be raised for a project while waiting for other sources of funding to be unlocked, or for an acquisition to be closed quickly without missing an opportunity.

Real estate lending crowdfunding is also very attractive to investors. Indeed, investing in real estate has always been one of the most coveted investments, but it normally requires large amounts of capital and imposes heavy management burdens. With crowdfunding, these two obstacles are eliminated, because the investment is divided among several people and a small amount is sufficient for each; in addition, the management charges remain with the company that owns the project. What's more, investment in real estate is something very concrete, it is understandable to everyone and tangible, unlike investment in new technology, for example.

Lending crowdfunding in Italy and Europe

In both Italy and Europe, lending crowdfunding is the fastest-growing sector in the 2020-2024 four-year period, driving the crowdinvesting market. This mainly concerns real estate. The Politecnico di Milano Crowdinvesting Observatory for Italy and the Crowdfunding Research Center for Europe are the reference points to look to for up-to-date data on industry trends.

Some recurring and significant features of this type of crowdfunding:

- Young entrepreneurs prefer lending crowdfunding.

- Those who do lending crowdfunding often do more than one campaign.

- In lending crowdfunding there is that phenomenon that is absent in other types of crowdfunding, namely the presence of usual investors, who invest in multiple campaigns. This is not strange: the rapid termination of the relationship with the proposing companies and the short-term return on interest stimulate recurring investment and reinvestment of the same interest collected. This aspect is also an important marketing lever for bidding companies doing a lending crowdfunding campaign, and proper investor retention paves the way for successful completion of multiple campaigns.

Do you need support in preparing a successful crowdfunding campaign and seeking potential investors for your project?

Turbo Crowd can accompany you throughout the process, from organizing the precrowd to closing the collection, developing effective and innovative marketing strategies to best promote your campaign.